|

Tuesday 5th May 2026 |

Text too small? |

Earnings Beat

Global

US equities finished the week mixed, with strength in Tech offsetting weakness in industrials. The S&P 500 rose 0.3%, the Nasdaq gained 0.9%, both closing at record highs, while the Dow Jones slipped 0.3% as defensives and cyclicals lagged.

Day 65 of the US-Iran conflict, Iran has proposed a new 14-point plan to the US to end hostilities in the region. President Trump posted on Truth Social “I will soon be reviewing the plan that Iran has just sent to us, but can’t imagine that it would be acceptable in that they have not yet paid a big enough price for what they have done to Humanity, and the World, over the last 47 years”.

Axois revealed that Iran’s suggestions included setting a one-month deadline on talks for a deal to reopen the Strait of Hormuz, ending the US naval blockade and the fighting in Iran and Lebanon altogether. Iran’s Tasnim News Agency called the proposal a complete end to the conflict within 30 days, saying the plan reiterates earlier demands, although the issue over the nuclear programme hasn’t been mentioned.

Major OPEC+ producers, led by Saudi Arabia and Russia, agreed to a small increase in their official June output quotas, adding around 188,000 barrels a day across seven countries. This comes on the heels of the United Arab Emirates’ surprise exit from OPEC effective 1 May, but the quota change is largely symbolic as the group cannot implement the increase while the Strait of Hormuz remains blocked.

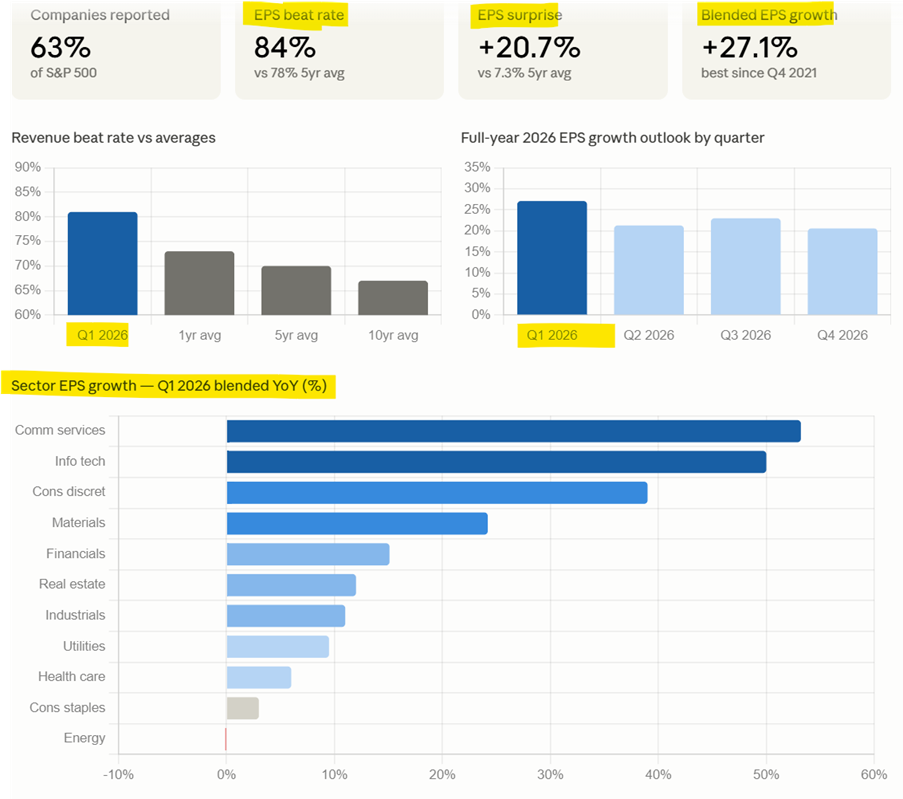

About two thirds of S&P 500 companies have now reported earnings, giving investors a solid read on the US corporate backdrop. Apple dominated Friday’s focus, with particularly strong results in its higher margin Services business and an improved gross margin profile, while iPhone sales were slightly better than expected.

Management highlighted exceptional demand for the new iPhone 17 lineup, noting that supply constraints rather than weak end demand are the main factor limiting current sales. Despite those bottlenecks, Apple guided more confidently for the coming quarter than the market had anticipated and paired that with the announcement of a massive US$100 billion share buyback, reinforcing confidence in its earnings outlook and balance sheet strength.

The US earnings season is running much stronger than usual across almost every metric. Companies are comfortably beating expectations now, and the outlook for 2026 is for very robust profit growth. So far, 84% of companies are beating EPS estimates, well above the 5 and 10 year averages and the highest beat rate since mid 2021.

The “Mag 7” is a key driver: their earnings growth has jumped to around 61% versus initial expectations near 22%, underscoring that the AI related trade remains very much intact, with NVIDIA’s result still ahead.

S&P 500 Earnings Report

New Zealand

The NZX 50 finished the week on a high note, adding a further 1.0% gain to the index at the close of the market. Top gainers on the day included Fletcher Building, which rallied 3.9% Mainfreight, which gained 3.4%, and Chorus, which finished up 3.0%. Underperformers included Sky TV (-2.5%), Gentrack (-1.3%), and Channel Infrastructure (1.3%).

The NZ REIT index managed a late-month rebound in April, finishing up 0.6% and outperforming the broader NZX 50 gross index, though property names remain under pressure year to date with the REIT index still down 8.8% versus a 4.8% fall for the wider market. Within the sector, Vital Healthcare Property, Property for Industry, and Stride Property led the gains, while Argosy, NZL, and Asset Plus lagged.

Centrix data show business failures are mounting, with 286 companies going into liquidation in March – the highest March tally since 2015 and part of a wider trend that has pushed annual liquidations above 3,000, up around mid teens percent year on year. Construction and hospitality remain among the hardest hit sectors, and insolvency specialists note that the first quarter of 2026 is tracking at the highest level of corporate appointments in about 15 years, echoing post GFC stress.

Methanex is signalling that its New Zealand gas contracts are now an asset in their own right, not just feedstock for methanol. On its Q1 call, the CEO said the company is “looking at all options” to monetise its NZ gas position, explicitly flagging a choice between running it through its Taranaki methanol plants or simply on selling gas into the domestic market. With contracts in place through to 2029, Methanex has several years of optionality: in tight supply periods, it has already shown it can earn attractive returns by diverting gas to electricity generators, and that dynamic is likely to continue if local gas remains scarce and prices stay firm.

Lastly, workers at the Taiwai Point aluminium smelter will take industrial action starting from today, following unsuccessful bargaining negotiations after more than two years of failed pay and conditions talks that started in 2024. Around 185 union members plan a series of short strikes and work restrictions rather than a full shutdown, marking the first strike at the site in decades and raising the risk of disruption at one of Southland’s biggest employers, while mediation is set to resume later in May.

Australia

The Australian ASX 200 snapped its eight-day losing streak by eking out a 0.7% gain to start the new month. Helping prop up the index were the heavy miners, surging on gains in iron ore prices, while gold miners also rallied.

Looking at individuals, Qantas gained 0.8% after flagging that capacity reductions will now run into the 2026-27 period, a move the market read as supportive for yields and pricing discipline even as demand normalises. Coles jumped 3.7% on an in line grocery trading update that reassured investors margins are holding up, with the absence of formal guidance not enough to dampen relief that it avoided the kind of negative surprises seen elsewhere in food retail.

At the weaker end of the tape, ResMed slid 3.5% even after posting another strong third quarter of double digit revenue and earnings growth, as investors stayed focused on GLP 1 weight loss drug risks and rising operating costs rather than the beat on margins and EPS. ANZ fell 2.8% after a mixed 1H26 result: revenue was softer than hoped and margin pressure lingered, but this was partly offset by good cost control and still low credit impairment charges, with no increase in standardised provisions, leaving the market unconvinced about near term earnings momentum.

Looking ahead this week, the primary focus will be on the RBA rate decision tomorrow, where a third straight hike is expected, a hawkish message from the Governor, and forecasts that keep the door open to at least one more move, most likely in August.

Globally, markets will stay fixated on the Iran war backdrop, a run of Fed speeches that may shed light on the recent 8–4 split and how policymakers are thinking about higher oil, plus US labour, inflation expectations and sentiment data due late in the week.

The New Zealand key labour force report will also be in focus, with consensus pointing to an unchanged unemployment rate.

No comments yet

June 11th Morning Report

SKO - Leadership Update

June 8th Morning Report

RBNZ announces decision on use of the word "bank"

June 2nd Morning Report

IKE - FY26 Financial Results

Chorus submits 2025 fibre regulatory report

SPG - FY26 Annual Results

PYS - PaySauce FY26 Full Year Result and Annual Report

IFT - Infratil Full Year Results for the year ended 31 March 2026

© Copyright 1997-2026 MoneyOnline Ltd - All Rights Reserved