|

Monday 15th June 2026 |

Text too small? |

Time and Place

Global

US equities climbed overnight, adding to a volatile week of risk-off trading, conflict, and IPO anticipation. President Trump once again signalled a deal is near with Iran, calling off planned strikes and refuelling hopes for an end to the war. Oil fell, while the three major indices advanced in tandem. The S&P 500 finished up 1.8%, the Nasdaq 2.5%, and the Dow 1.9%.

The US launched a second consecutive day of strikes against Iran, while Iran responded with strikes targeting Bahrain, Kuwait and Jordan. President Trump, losing patience, posted on Truthsocial, “The United States will be hitting Iran…VERY HARD TONIGHT. At some point in the not too distant future, we will be taking Kharg Island, and other oil infrastructure points, and assume total control of their Oil and Gas Markets, much like we have with Venezuela”.

In the last few hours, Trump later took back his statement, saying “Based on the fact that discussions with the Islamic Republic of Iran have been brought to the highest level of Iranian leadership and approved, I have…cancelled the scheduled strikes and bombings against Iran this evening. Discussions and final points have been, in both concept and great detail, approved by all parties involved, including the United States, Israel, Saudi Arabia, UAE, Qatar, Turkey, Pakistan, Bahrain, Kuwait, Jordan, Egypt, and others. The Naval Blockade will remain in full force and effect until this Transaction is finalized — Time and place of the signing to be announced shortly.”

Positive sentiment quickly spread across the market on the news, rallying in late-afternoon trade as investors piled back into risk-on equities. Bond yields fell, with the 10-year rate declining 9bps, while Brent crude dropped to USD90 per barrel.

SpaceX has achieved a historic milestone by launching the largest IPO ever, raising an unprecedented $75 billion in capital. The company sold 555.6 million shares at $135 per share, which gives SpaceX a total market value of $1.77 trillion. This massive valuation puts founder Elon Musk on the brink of becoming the world's first trillionaire, as his ownership stake in SpaceX, combined with his other holdings like Tesla, would push his wealth beyond the threshold once the IPO pricing is finalised and trading begins tonight NZT.

Elsewhere, the European Central Bank (ECB) made a significant policy shift by raising interest rates for the first time since 2023, marking a decisive move away from its previous accommodative stance. ECB President Christine Lagarde delivered a stark warning that inflation driven by the Iran war is no longer confined to energy prices alone but is spreading to other parts of the economy. ECB officials are not ruling out another rate hike, with the next potentially being as early as July.

New Zealand

The NZX 50 weakened, reversing the gains from the previous session to fall 0.4% with the index trading below the 200-day moving average. The biggest detractor on the day was Scott Technology, which lost its rally momentum as investors locked in profits, falling 4.2%. Infratil declined 1.9%, and Auckland International Airport slip 1.8%. Top gainers on the day included Skellerup (+3.3%), Hallenstein Glasson (+2.0%, and Briscoe Group (+1.8%).

New Zealand Ministry of Primary Industries (MPI) issued China an Official Importer and Manufacturer Approval amendment, introducing stricter testing requirements for cereulide toxin in infant formula to introduce more rigorous screening and quality control measures for infant formula products destined for the Chinese market. This regulatory change adds compliance costs and operational complexity for a2 Milk, potentially affecting their production timelines and supply chain efficiency.

Further to this, analysts reveal a desktop scan of Chinese online retail platforms confirms that China-label stock (products specifically labelled and packaged for the Chinese market) is experiencing widespread shortages across many e-commerce storefronts. For a2 Milk, this creates a challenging situation in which regulatory compliance requirements are tightening while its product availability in the Chinese market is diminishing. The combination of stricter testing mandates and visible stock shortages indicates potential headwinds for a2 Milk's key infant formula business in China.

Elsewhere, NZ’s renewable energy sector has achieved a significant milestone, with renewables generating 94.5% of all electricity in the quarter ending March 2026, according to MBIE's latest Energy Quarterly report. This represents a substantial increase from 83.2% in the same quarter last year.

The 94.5% renewable generation rate puts New Zealand among the world's leaders in clean electricity production, surpassing most developed nations. This achievement aligns with the country's broader environmental targets, including its commitment to net-zero carbon emissions by 2050. The rapid improvement also suggests that the renewable energy transition is progressing faster than previously anticipated, with the remaining 5.5% of electricity still coming from non-renewable sources.

Australia

The ASX 200 followed the trend, taking back gains from the previous session to fall 0.2%. Energy, Consumer Staples, and Healthcare were the best performers, while Industrials, Financials, and Tech were the laggards.

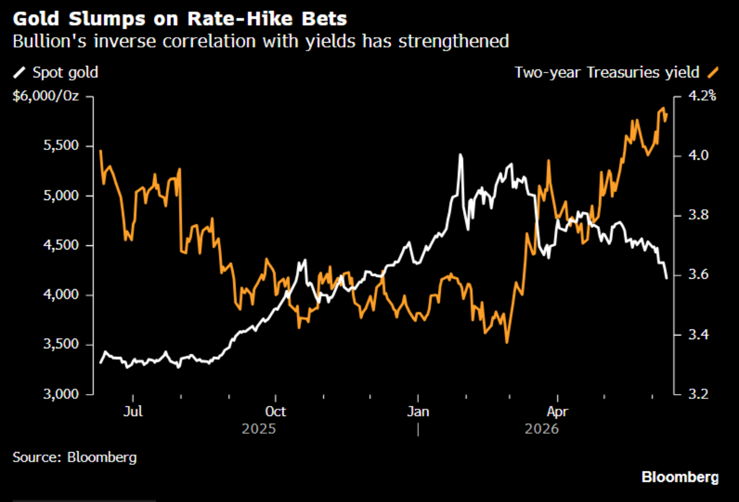

Materials turned higher after starting the day in the red, with some strength returning to battered gold stocks, despite the overall precious miners still declining 0.8%. The precious metal is now below US$4,100/oz, down 22% from US$5,200/oz in early March amid inflation concerns.

Bottoming the index, Alcoa fell 8.3% after its CFO delivered a stark warning about the company’s Alumina segment. The CFO stated that the Alumina business was "underwater" in Q2, meaning it's operating at a loss. The CFO also flagged additional costs that weren't included in analyst consensus estimates.

Amongst Healthcare, CSL continues its recovery, surging another 4.2% and gaining 15.4% over the last five sessions. Banks were weaker, weighed down by Westpac, which fell 2.6% after its consumer strategy update, where it announced that loan applications had fallen 20% since the budget changes were announced.

Tech was the worst overall, falling 2.2% as investors continued to position themselves ahead of SpaceX’s IPO, anticipating capital rotating away from already-held tech stocks to fund purchases of SPCX shares. In the space, selling was concentrated in Nextdc (-4.2%) and Xero (-3.6%) as the leading decliners. Megaport stood out as a positive outlier, rising 3.6%.

No comments yet

FPH 2026 Notice of Annual Meeting and Voting Form

CNU - Q4 FY26 Connections Update

SPK - Spark announces appointment of Chief Operating Officer

SKC - Asset Monetisation Programme Update - The Grand Hotel

VCT - Full year results date & investor webcast details

ANZ - Air New Zealand 2026 Annual Results Webcast Details

SKC - Asset Monetisation Programme Update

July 17th Morning Report

MEL - Meridian Energy monthly operating report for June 2026

Devon Funds Morning Note - 15 July 2026

© Copyright 1997-2026 MoneyOnline Ltd - All Rights Reserved