By Anthony Quirk

|

Friday 2nd June 2006 |

Text too small? |

A key reason for this is the reversal of speculative excesses in some markets. However, there is also a growing concern that the �goldilocks� US and global economic outlook (good growth without associated inflationary issues) may not occur going forward. Instead there are concerns that a scenario of too much growth and inflation will lead to continuing co-ordinated Central Bank interest rate rises. Also, there are some in the market who are fearful of stagflation (high inflation and interest rates and low growth).

After the incredible returns from various global markets over the past few years (and the significant speculation entering some markets) a sell-off is not a huge surprise; although very difficult to time exactly! But is this the start of a bear market phase or just a necessary correction to release some of the steam from over cooked markets?

The case for this being �just� a correction only is as follows:

|

2002a |

2005a |

2006f |

2007f |

|

|

United States |

1.6 |

3.5 |

3.5 |

2.6 |

|

Euroland |

0.9 |

1.4 |

2.0 |

1.7 |

|

Japan |

-0.3 |

2.7 |

3.2 |

2.9 |

|

Australia |

4.0 |

2.7 |

3.7 |

3.5 |

|

China |

8.2 |

9.9 |

9.6 |

9.1 |

|

World |

2.8 |

4.2 |

4.3 |

3.8 |

|

New Zealand |

4.8 |

2.2 |

1.2 |

2.4 |

Source: Statistics NZ, RBNZ, GSJBW

|

Price/Cash Earnings |

||

|

Region |

Current |

20 Yr Range |

|

US |

12.2 |

6.3-19.7 |

|

Japan |

10.8 |

7.1-18.4 |

|

MSCI Europe |

8.4 |

6.6-16.0 |

Source: Capital International

The case for this being the start of a bear market is:

So how does New Zealand look under these varying global scenarios?

While the New Zealand sharemarket has done very well over the past three years (23% compound growth for the NZX50 Index), it does not seem to have been caused by any speculative bubble. We have been relatively immune from any extreme excesses of the commodity and emerging market boom, just as we were from the dot com bubble bursting. Having said this we were vulnerable to a sell-down given the significant upwards P/E re-rating we have enjoyed relative to the rest of the world (as highlighted in last month�s commentary).

While we are going through a recession at present, it is a shallow one and we do not look like we are heading for a hard landing. Instead the positives of continuing strong global economic growth and a weaker Kiwi dollar means that the export sector should be robust. This is the traditional way for the New Zealand economy to come out of a recession (a pick up in the country before moving into the city) and it looks like being repeated in 2007. Any further lift from a recent pick up in immigration will further help matters.

So my conclusion is that while we can expect more volatility over the coming months than the relatively low levels of recent years, the long-term outlook for global sharemarkets looks sound. One could try to time this by trading in and out of market fluctuations but for most investors I believe the best strategy is to keep to a long-term perspective as the rewards should be there � albeit not as stellar as they have been in recent years.

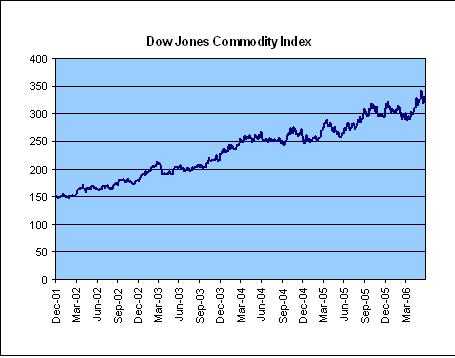

Source: Bloomberg

Anthony Quirk is the managing director of Tyndall Investment Management New Zealand Limited (Tyndall).

No comments yet

Opinion: Sorry Feltex saga has damaged reputations and confidence

Opinion: Commission investigation into Plus SMS will test credibility

Market Review: US housing downturn a warning for New Zealand?

Opinion: Government wants better co-ordination between regions

Opinion: A flutter on Sky City shares may become more of a gamble

Opinion: Slowdown? What slowdown? Economic data tells two stories

Opinion: Electricity investment uncertainty after mixed messages

Market review: At the crossroads

Opinion: This will transform the economy won't it? Yeah right

Opinion: Sharemarket performance as bleak as the weather

© Copyright 1997-2026 MoneyOnline Ltd - All Rights Reserved