By Anthony Quirk

|

Friday 7th July 2006 |

Text too small? |

Thus the market anticipated last week�s US rate hike (the 17th straight rise) and if rates had not been raised, after such a co-ordinated set of speeches expressing concern on inflation, it would have left the Federal Reserve with zero credibility. Moreover there seems to be co-ordinated Central Bank tightening underway, from countries as diverse as the US and China through to Korea, Sri Lanka, Peru and Turkey. New Zealand seems to be one of the few exceptions to this, given we are at a different stage of our economic cycle.

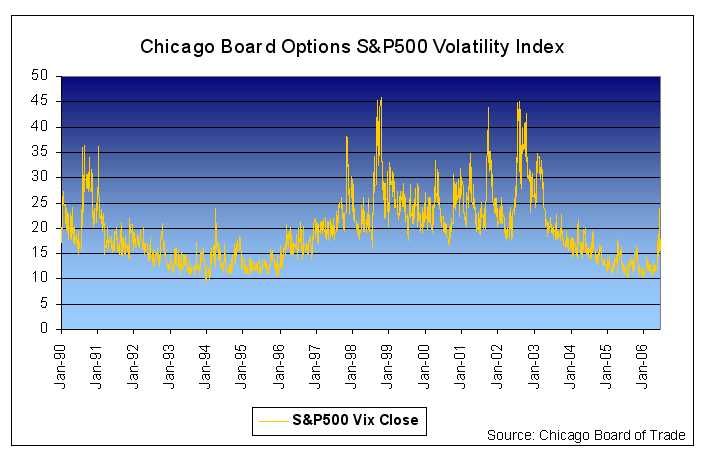

After a period of relatively low volatility for the past three years sharemarkets have gyrated recently. For example, in June the three major US sharemarket indices hit new lows for 2006 and then posted their biggest one-day gains in years! The increased market volatility and heightened investor concerns are shown in the chart below. This shows the Chicago Board Options S&P 500 Volatility Index (VIX) rising from early May after being at historically low levels over the past few years, before settling to more normal levels by the end of June.

The increased volatility, combined with inflation concerns and general uncertainty, means investors required a higher return from equities to compensate. That is, the discount rate used to value companies rose. If the earnings outlook stays constant then sharemarket values fall, and that is what we experienced in May and June.

So two related key issues from here are:

So my conclusion is similar to last month�s commentary. Namely that, subject to no external shocks (including the Federal Reserve over tightening), I do not believe this is the start of a bear sharemarket but merely a healthy correction that was needed given the extraordinary returns from shares over the past few years.

To see how the numbers stacked up for various markets around the world in the past month and over the year, visit our Monthly Market Review here

Anthony Quirk is the managing director of Tyndall Investment Management New Zealand Limited (Tyndall).

No comments yet

Opinion: Sorry Feltex saga has damaged reputations and confidence

Opinion: Commission investigation into Plus SMS will test credibility

Market Review: US housing downturn a warning for New Zealand?

Opinion: Government wants better co-ordination between regions

Opinion: A flutter on Sky City shares may become more of a gamble

Opinion: Slowdown? What slowdown? Economic data tells two stories

Opinion: Electricity investment uncertainty after mixed messages

Market review: At the crossroads

Opinion: This will transform the economy won't it? Yeah right

Opinion: Sharemarket performance as bleak as the weather

© Copyright 1997-2026 MoneyOnline Ltd - All Rights Reserved